The other day, I got an email from Chase, letting me know about some offer I had waiting for me, provided I downloaded Chase Pay, their digital payments app. When I went to the App Store and searched for “Chase Pay,” I discovered three rather distinct Chase banking products, which, taken together, nicely represent a three-tier segmentation of their market.

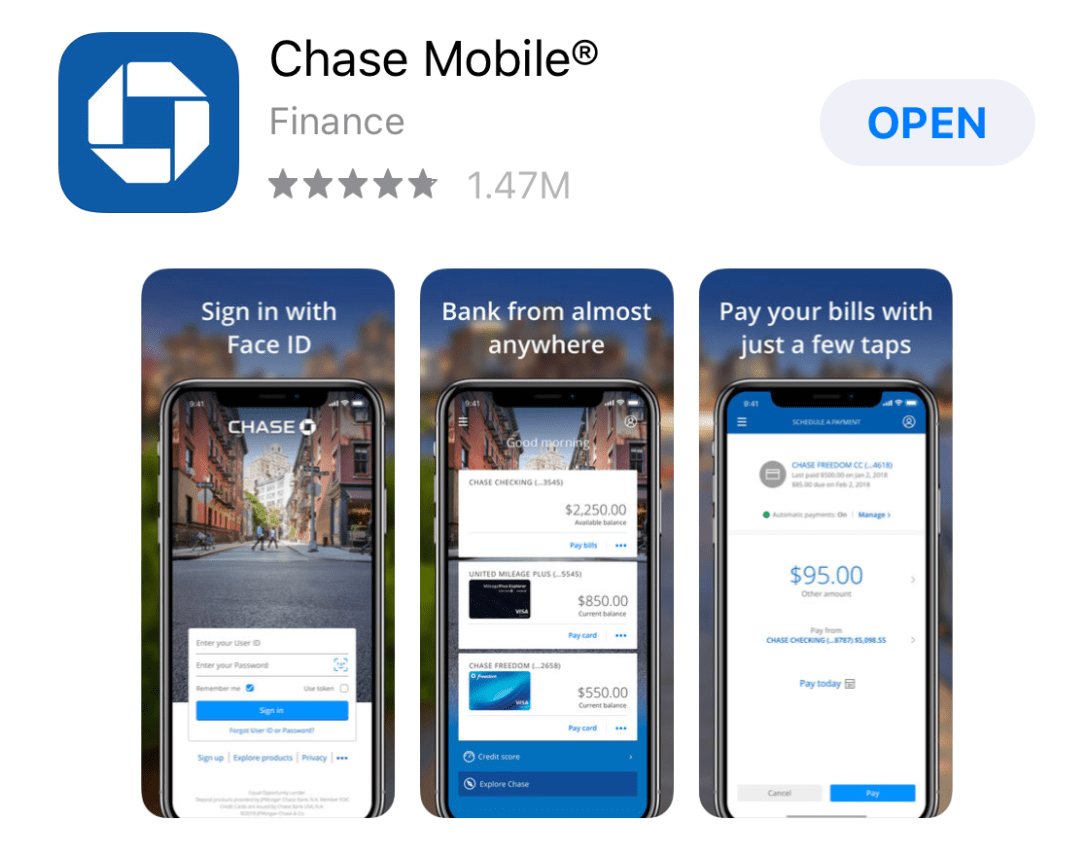

- The first — and most common product, I assume — is Chase’s vanilla banking app, used by several million people across the US. You can tell by the details in the sample images of the app: The background image is the middle of a street in lower Manhattan (pretty sure it’s SoHo, but corrections are welcome). The foreground transactional data are of two mid-tier credit cards (a United Card, and a Freedom Card, both of which have account balances under $1,000), and a checking account with a fairly standard balance ($2,250). The one sentence descriptors, “Sign in with FaceID,” “Pay your bills with just a few taps,” fit generalized use cases, like paying bills or seeing credit card balances.

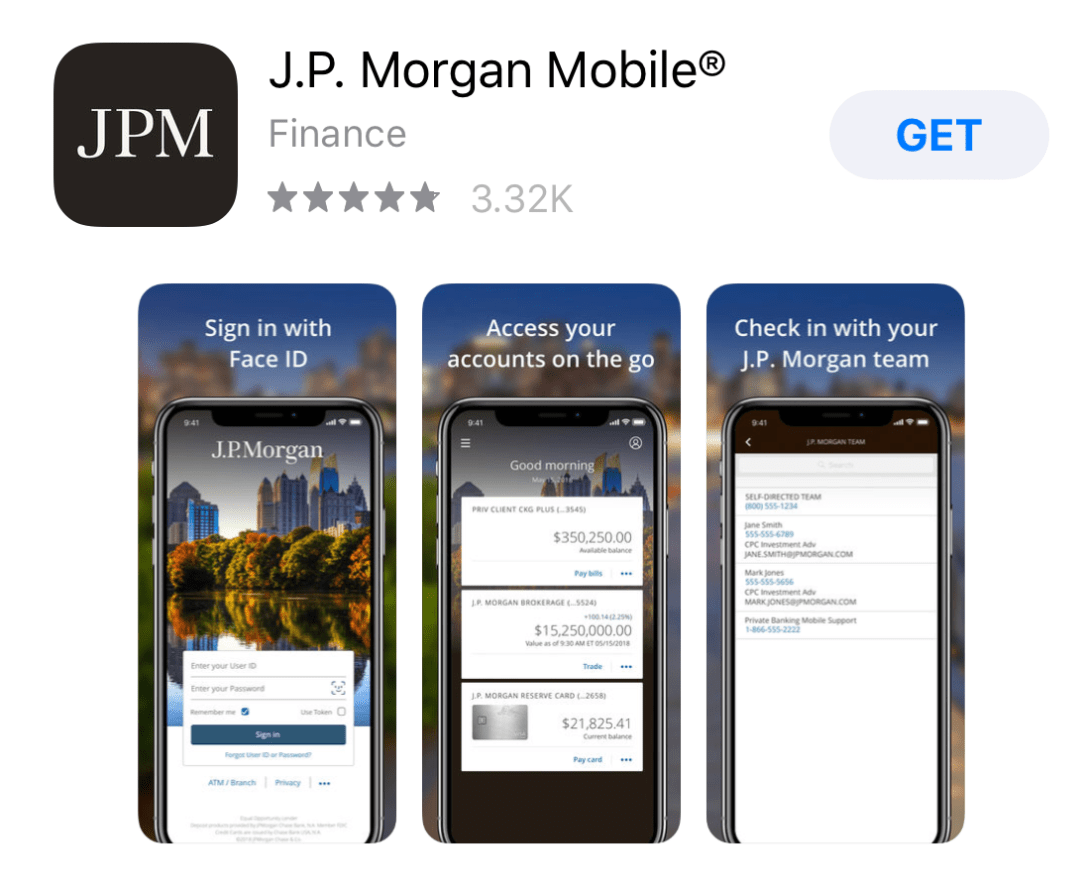

- One of the next results you get — again, still just from plugging in the term “Chase Pay” into the App Store — is JP Morgan Mobile, the private banking arm of the Chase family.

You’ll notice some strategically different details here. The background is no longer a street in downtown NYC. Rather, the background image is of buildings on the Upper West Side, as seen from the Central Park Reservoir — an admittedly tonier neighborhood than the (still expensive) part of NYC that was featured as the background image in the regular Chase Mobile app.And, you’ll notice, the graphics and microcopy are different. Where the Chase App simply used its logo for the app icon, JP Morgan Mobile uses a stalwart “JPM” in serif font on a plain black background.

Moreover, take note of the account balances. Even though the interface is the same, a lot of the smaller details are quite different. The private client in question has a cool $350k in cash, a $15m portfolio, and a $21,825 balance on her credit card. Moreover, the call-to-action on the final pane isn’t about paying bills, it’s about checking in with your private banker and your investment advisors. It even shows (fictitious 555-number) data, to reassure high rollers that, yes, you will get a direct line to a banker.

- Perhaps more interesting than doing deep dives into what neighborhood of New York represents what socioeconomic segment, is taking a look at another Chase app that popped up for me. Meet Finn.

Unlike Great-Grandma JP. Morgan or Uncle Chase, Finn very obviously enjoys a good taco, and is partial to emoji every now and then. Getting down brass tacks, you’ll notice a few things.

Unlike Great-Grandma JP. Morgan or Uncle Chase, Finn very obviously enjoys a good taco, and is partial to emoji every now and then. Getting down brass tacks, you’ll notice a few things.Where before the backgrounds were NYC-themed, Finn prefers a more colorful, variegated background. Is this because Finn can’t afford NYC rent? Does Finn secretly live with his folks in Northern New Jersey? Or maybe Finn is way out in, like, Astoria, and is just papering it over by slapping a colorful filter on his Instagram photos so you can’t really tell where they were taken.

No matter where Finn lives, you’ll notice that his plastic of choice is a debit card, which is geared to appeal to notoriously credit card-averse millenials. Finn’s look-and-feel are colorful and rounded, where Chase and JPM were, well, square. The CTAs of “Save that Money” and “Get Involved” speak to the fact that millenials are earning less than their parents did at this age, but also maintain a strong social ethic.

On a microcopy level, you’ll see that Finn enjoys going to concerts, and the app allows users to budget their income on a monthly basis, to save up for the good stuff. The expenditure on the far right pane features a $48 tab at a nearby pub (what were you getting, a single malt!?) along with the requisite emoji that now accompany all finance apps aimed at young people — ahem, Venmo.

One small detail I did notice is that Finn does seem to have a higher balance ($3,450) than Uncle Chase. I assume that, because Finn is most likely pulling espresso shots without a 401(k) plan in place, he probably doesn’t have diversified assets beyond what you can see in the images. But I’m just speculating here.

Important to note is that Finn is mobile-only. Going to Chase’s site directs you back to the App Store.

Finn very much fits the mold of other, new finance apps, and perhaps most closely resembles Goldman Sach’s newish, one-name-only consumer banking option, Marcus, as well as other finance apps like the aforementioned Venmo, as well as the super-popular Robin Hood investment app.

What Chase’s variety of banking products — and their respective apps and design convey — is that it’s an interesting time to be in finance, and that the growth of younger demographics (albeit with substantially less disposable income), creates challenges that are interesting to see addressed on both product and marketing levels. 🌮